Article

11 min read

Banking process automation is transforming business as usual for financial institutions by creating systems that can think and act consistently under complex regulations.

Banks used to rely on manual approvals. Now they use rule-based workflows that connect lending, payments, and compliance in real time.

According to the European Central Bank's horizontal assessment on process automation in banking, 83% of banks believe that automation is key to reducing operational costs. They see these savings coming mainly from modernizing outdated IT systems. These systems keep an eye on transactions as they happen, keep audit-ready records, and give management a clear picture of what's happening across core banking, CRM, and mobile channels.

Key Insights:

- Automated approvals and digital signatures can speed up your processes by approximately 80%, providing your customers with a better experience.

- Using orchestration (faster with low-code) lets you put together core banking, CRM, internet banking, and APIs into one flow that works together.

- Whenever a process is carried out, it automatically checks that it's compliant with PSD2, AML, and GDPR requirements (clearing most transactions in under 10 seconds).

- Instant payment networks such as SEPA Instant and Moldova’s IPS (MIA) already process billions of euros and over 13 million instant transfers yearly, with 750,000+ users.

- Using automation helps you see more clearly how much money is available, reducing any risks to the way the business is run, while making financial reporting more accurate.

Why is it important to automate banking processes?

These days, being efficient isn't just about doing things the right way. It's about showing they're right at the moment. In the past, regulators were happy to wait for evidence that something met the required standard. These days, customers expect instant confirmation.

That's where automation can help. It closes the gap by checking that rules are being followed in real time, logging each action automatically for speed and accountability.

Now, they're using technology to keep up with the demand for accountability (what happened behind the scenes). All activities are recorded in real time, from Know Your Customer (KYC) verification to payment authorisation, ensuring immediate access for regulators and internal teams to review actions.

This level of transparency is what builds trust. That’s why it’s critical to be transparent and prove you’re following the rules on the spot, with every breath of the system.

"Automation doesn't replace people — it replaces waiting." — Dumitru Gnaciuc, Engineering Manager, EBS Integrator.

Workflow pipelines as a competitive advantage

In regulated markets, organisations using automated workflow management grow 35-50% faster and adapt to legal changes 5-10x quicker than than their peers that use manual processes. By embedding compliance logic into every digital transaction, these organisations cut operational risk by 80–95% while sustaining 99.9% service uptime — even under live audits or system failure.

The regulatory compliance costs that were once a burden have now become a valuable asset.

Banks no longer experience audit panic or undertake compliance sprints; they simply absorb governance and regulatory changes in real time.

How process automation in banking works

Whether it’s approving a loan or verifying an applicant’s identity, every banking process still follows the same structure: data is collected, validated, and recorded for review.

What’s changed is the coordination behind it.

Teams used to do seventeen manual steps, but now automation does everything digitally, linking customer data, risk checks, and approvals into one system.

You can see every step, it's all compliant and ready for audit, and there's no need to re-enter or move data between platforms, which makes things simpler.

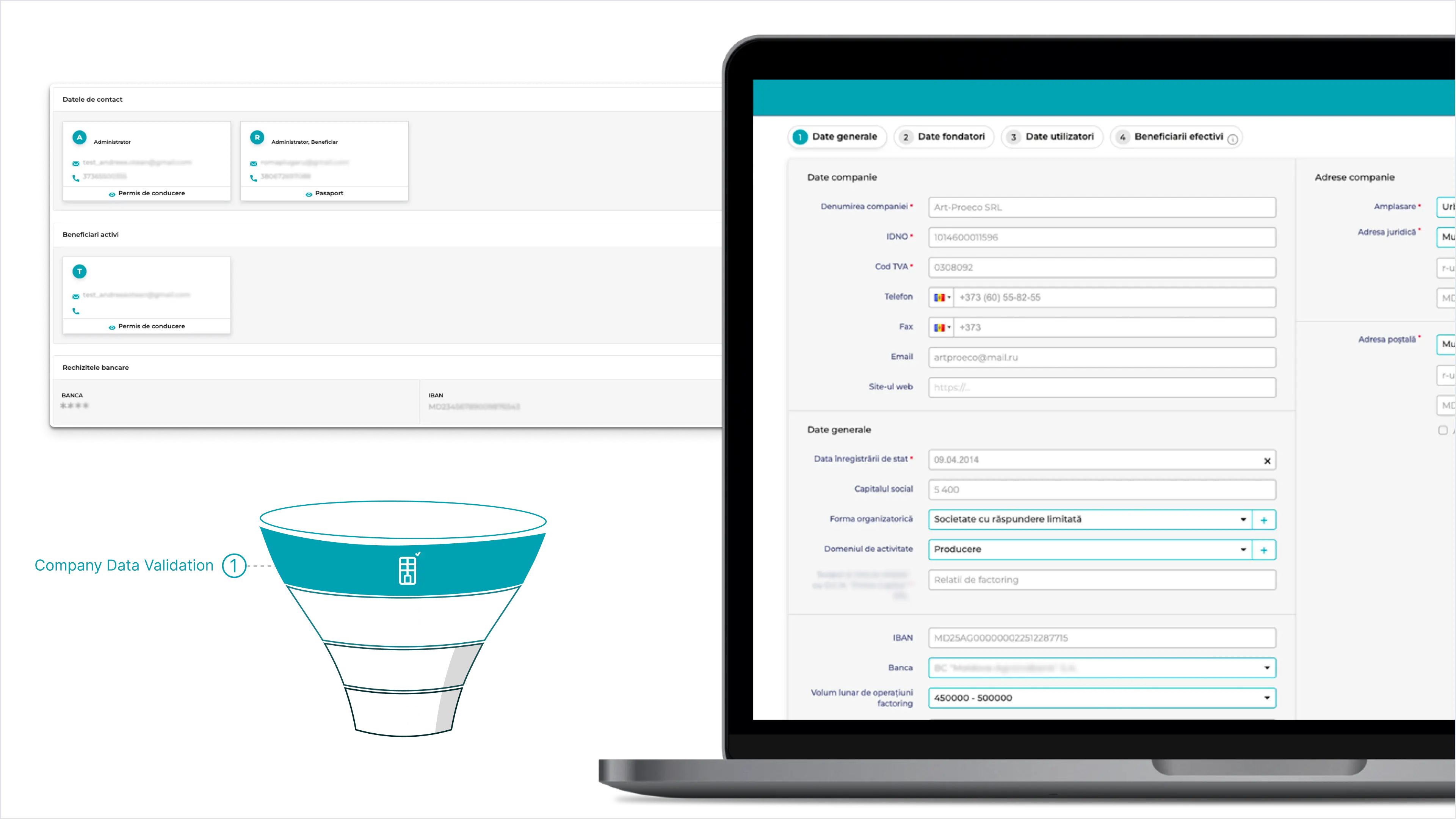

Orchestrating core banking, CRM, and onboarding

Modern workflow automation brings together core banking, CRM, and digital onboarding. It does this in one continuous process.

We've had a chance to put this into practice on a factoring project, where we replaced manual coordination with automation.

All the credit assessments, invoicing, and approvals now happen in one CRM-driven workflow, which makes the process up to 70% faster and tracks every action for audit.

Low-code orchestration, powered by platforms like ours (EBS.io), takes this even further. It gives banks the edge of being able to adapt quickly to new rules or product launches without disrupting existing systems.

"Time is turned into insight by automation. Every second that is saved becomes a data point that can be learned from." — Dumitru Gnaciuc, Engineering Manager, EBS Integrator.

Compliance by design in financial workflows

Modern banking automation is surely making processes faster and more efficient, but more importantly, it keeps them compliant by default.

Instead of stopping at every stage to perform checks manually, banks now design workflows with regulatory logic that validate each action automatically and keep a record of it.

It's all done automatically, whether that's approving a loan, verifying someone's identity, or transferring funds. And the best part is that it'll also keep a full record of everything that's happened.

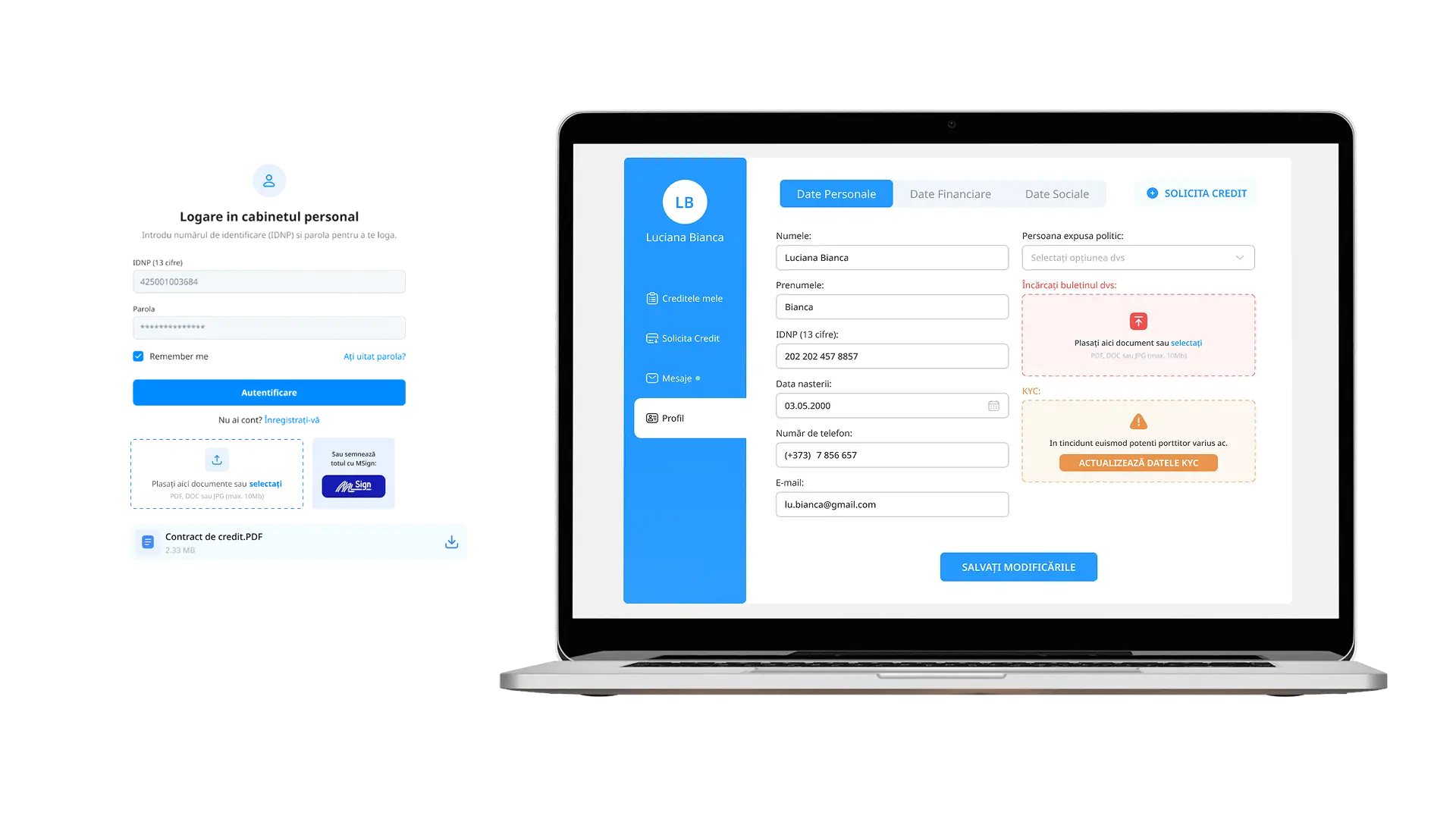

Embedding PSD2/SCA and KYC/AML checks

In regulated environments, these layers are all dependent on each other, so we implement them as one data flow, not as separate checkpoints.

PSD2 and Strong Customer Authentication (SCA) work with Know Your Customer (KYC) and Anti-Money Laundering (AML) controls. Basically, this means identity verification, authentication, risk scoring, and recordkeeping all happen in one automated sequence. We saw this approach really pay off when we helped a local bank switch to PSD2 and Instant Payment System (IPS) compliance.

By adding payment logic, strong authentication, and risk validation straight into the transaction flow, the bank got real-time P2P and RTP transfers, full audit visibility, and 20x growth in processed transactions—all while keeping up with continuous compliance and security.

Continuous governance and reliability

You see real change when compliance is part of the day-to-day routine. It's not something that just happens on its own.

All decisions are automatically recorded, including who was involved, what was done, when it happened and which rule was broken.

Teams see the same data at the same time, and any issues are spotted before they turn into problems.

Basically, that's how you go from "checking" compliance to actually putting it into practice — regularly, openly, and prepared for change.

From operations to financial intelligence

Once automation has things under control, it can start to really shine — with insights like you wouldn't have thought possible.

These days, banking is about more than just automating tasks. It's also about learning from the data that those systems produce all the time.

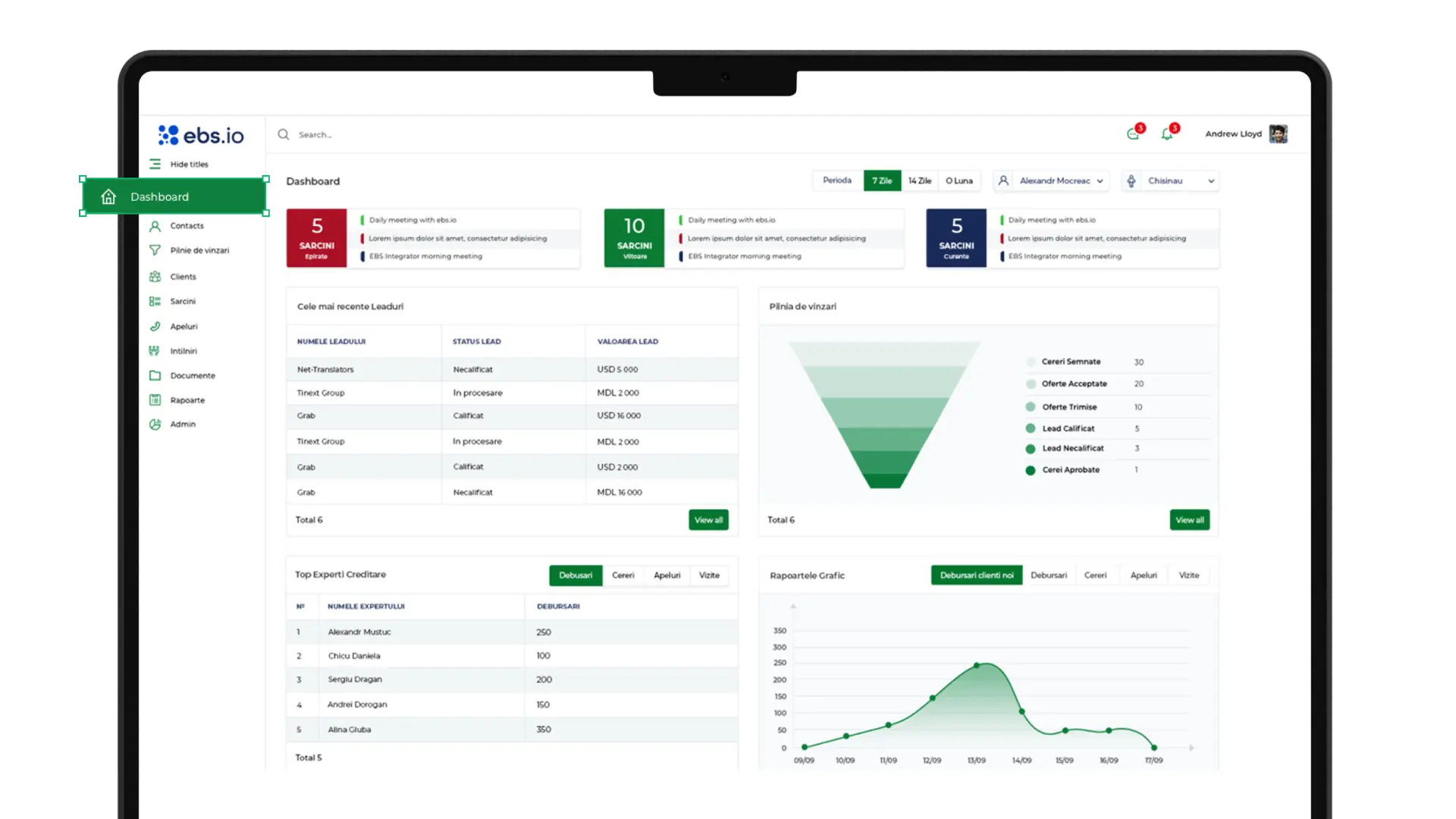

For a microfinance lender we deployed a CRM with real-time dashboards (the one below) embedded directly within the end-to-end workflow pipeline, linking onboarding, credit scoring, loan disbursement, repayment tracking and compliance validation. So, instead of having all those raw transaction logs, now they're more like handy tools for decision-making, giving teams a clear view and control of the whole lending cycle.

The credit team could see client activity, loan statuses, and repayment progress right away, turning their records into clear, actionable intelligence.

Where dashboards used to track performance, they now guide decisions.

Data-driven adaptation

Data is no longer just a record of what happened — it’s a guide for what to do next.

When automation links customer journeys, transactions, and support channels, it creates a feedback loop that helps banks adapt in real time.

Institutions use these insights to forecast demand spikes, refine service timing, and anticipate client needs before they’re voiced. It’s the same technology that once powered reports, now powering responsiveness — turning every interaction into a signal for smarter decisions.

Predictive banking & customer experience

Once data becomes reliable, prediction becomes practical.

By blending automation data with AI models, banks detect shifts in spending, early signs of credit risk, or moments when a client may need support.

These insights change how institutions prioritize work — teams move from chasing issues to anticipating them.

Customer experiences feel more personal because they’re timed to intent, not coincidence.

That’s how banks turn data that once explained the past into signals that quietly shape the future.

Instant payments and regional adoption

Across Europe, instant payment systems are becoming more and more popular (particularly evident in Eastern markets, where national infrastructures are undergoing rapid development). This means that processes can be automated to match the customer's pace, without compromising on compliance or control.

EU Baseline, SEPA Instant Payments

The European Payments Council (EPC) now treats SEPA Instant Credit Transfer (SCT Inst) as the baseline for real-time payments across the EU.

Transfers are processed in under 10 seconds, and the number of participants is increasing. 19 banks in Romania are already live on the SEPA Instant scheme, with payment volumes increasing over fourfold year on year.

Local Momentum

Moldova's new Instant Payment system is also going great. It has already been used over 750,000 times and handled over 13 million transactions in just 18 months. The total amount of Moldavian lei (MDL) processed by the system is MDL 4.8 billion. That's a strong sign that local infrastructure can make real-time account-to-account transfers happen across the country, and do it safely too.

They show that local adoption, when built on the right architecture, can move just as fast — connecting national innovation with European interoperability.

How to turn banking automation into a long-term advantage

These days, automation isn't just about saving time — it's how modern banks stay on the right side of regulations, are open about what they're doing, and keep their customers' trust.

Here at EBS Integrator, we've watched innovation become as normal as breathing once data starts flowing clearly across systems.

"Digitalisation only works if it's moving as fast as your decisions. If your systems can't respond in real time, it's not transformation, it's just decoration." — Dumitru Gnaciuc, Engineering Manager, EBS Integrator.

We help banks build systems that not only work, but also learn. If you're thinking about bringing compliance, customer experience, and operations together into one adaptive flow:

Share this article on:

More articles

Article

Technology

All Capabilities

Digital Transformation

Finance & Banking

9 min read

Financial technology, or FinTech, is revolutionizing the way we manage, invest, and spend money, making transactions smoother, faster, and more secure. From mobile payments to blockchain technology fintech is bringing financial services into the digital age and making life easier for businesses.

26 Mar 2024

Article

Digital Transformation

Business Strategy & Growth

8 min read

Many see digital transformation as a quick fix for outdated systems, but it’s much more than that. It’s about building smarter, stronger ways of working—operationally, technically, and culturally. This means ensuring teams not only use new technology but understand its purpose and value. Our CEO, Vitalie Aremescu, and Business Analysis Manager, Natalia Ciobanu, share their expertise in helping businesses adapt and thrive in today’s market.

20 Dec 2024

Article

IT Consulting

Business Analysis

Digital Transformation

6 min read

Learn how consulting has changed—and why it works better than traditional approaches. *Real examples from our porfolio included - showing how it solves problems others couldn’t.

22 Apr 2025